.png)

Bone Grafts And Substitutes Market By Product (bone Grafts Substitutes, Cell-based Matrices And Allografts) And Application ( Joint Reconstruction, Dental Bone Grafting, Trauma, Craniomaxillofacial And Spinal Fusion) - Global Industry Analysis And Forecast To 2023

Published On : July 2018 Pages : 190 Category: Biotechnology Report Code : HC071107

SEGMENTS & REGIONS:

- By Product: bone Grafts Substitutes, Cell-based Matrices And Allografts

- And Application: Joint Reconstruction, Dental Bone Grafting, Trauma, Craniomaxillofacial And Spinal Fusion

- Regions: North America, Europe, Asia- Pacific, Latin America, Middle East & Africa

Industry Outlook and Trend Analysis

The Bone Grafts and Substitutes Market was worth USD billion in 2017 and is expected to reach approximately USD billion by 2023, while registering itself at a compound annual growth rate (CAGR) of % during the forecast period. Bone grafts and substitutes are used to repair fractures in the bone, bone development, and osseous reconstruction as these materials are having osteoconductive and osteoinductive properties. These grafts and substitutes are made up from engineered and characteristic materials, and creature and human-obtained tissues. A perfect bone graft and substitute must be osteoinductive, biocompatible, bioabsorbable, and inexpensive. Thereby, these are commercially accessible for orthopedic applications, for example, spinal fusion, sports related injuries, and joint reconstruction. Substantial number of surgeries prompt ascent in demand for donation of musculoskeletal tissue and a lack of cadaver material.

Product Outlook and Trend Analysis

Allograft techniques decrease surgical time, hospital stay, and injuries involving a shorter injury recuperating time. Considering the aforementioned factors, the allograft method section is seen to be the favored significantly over the globe. Demineralized bone matrix is a kind of allograft, which has generally better osteoconductivity and osteoinductivity in comparison with different allografts.

Application Outlook and Trend Analysis

The spinal fusions fragment represented the biggest income share in 2017 and is foreseen to keep up its dominance amid the estimate time frame. Increasing demand for spinal combination fusions procedures among the aged populace is impelling the entrance of bone grafts among alternate applications. Moreover, wide accessibility of bone graft substitutes and enhancing reimbursement schemes for dental surgeries are some of the main aspects anticipated to boost the demand for BGS in dental applications.

Regional Outlook and Trend Analysis

North America was the main market and was trailed by Europe in 2017. Factors, for example, high levels of awareness in regards to commercially accessible products, higher expense on healthcare, and the accessibility of cutting edge medicinal services foundation added to the development of the market in these areas. Nonetheless, a demanding administrative structure and high treatment costs are testing the development of the market in North America and Europe.

Competitive Insights

The leading players in the market are Johnson & Johnson, Arthrex, Inc, Baxter International Inc., Xtant Medical Holdings, Inc., Wright Medical Group N.V., Zimmer Biomet Holdings, Inc., Stryker Corporation, Medtronic Plc., Musculoskeletal Transplant Foundation, and Integra Lifesciences Holdings Corporation. The major players in the market are profiled in detail in view of qualities, for example, company portfolio, business strategies, financial overview, recent developments, and share of the overall industry.

The Bone Grafts and Substitutes Market is segmented based on regions as follows-

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Russia

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Southeast Asia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Columbia

- South Africa

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- UAE

- Egypt

- Nigeria

- South Africa

- Rest of MEA

Some of the key questions answered by the report are:

- What was the market size in 2017 and forecast from 2017 to 2023?

- What will be the industry market growth from 2017 to 2023?

- What are the major drivers, restraints, opportunities, challenges, and industry trends and their impact on the market forecast?

- What are the major segments leading the market growth and why?

- Which are the leading players in the market and what are the major strategies adopted by them to sustain the market competition?

Market Classification

· Bone Grafts and Substitutes Market, By Product, Estimates and Forecast, 2014-2023 ($Million)

· Bone Grafts Substitutes

· Cell-based Matrices

· Allografts

· Bone Grafts and Substitutes Market, By Application, Estimates and Forecast, 2014-2023 ($Million)

· Joint Reconstruction

· Dental Bone Grafting

· Trauma

· Craniomaxillofacial

· Spinal Fusion

· Bone Grafts and Substitutes Market, By Region, Estimates and Forecast, 2014-2023 ($Million)

o North America

§ North America Bone Grafts and Substitutes Market, By Country

o U.S. Bone Grafts and Substitutes Market

o Canada Bone Grafts and Substitutes Market

o Mexico Bone Grafts and Substitutes Market

o Europe

§ Europe Bone Grafts and Substitutes Market, By Country

o Germany Bone Grafts and Substitutes Market

o UK Bone Grafts and Substitutes Market

o France Bone Grafts and Substitutes Market

o Russia Bone Grafts and Substitutes Market

o Italy Bone Grafts and Substitutes Market

o Rest of Europe Bone Grafts and Substitutes Market

o Asia-Pacific

§ Asia-Pacific Bone Grafts and Substitutes Market, By Country

o China Bone Grafts and Substitutes Market

o Japan Bone Grafts and Substitutes Market

o South Korea Bone Grafts and Substitutes Market

o India Bone Grafts and Substitutes Market

o Southeast Asia Bone Grafts and Substitutes Market

o Rest of Asia-Pacific Bone Grafts and Substitutes Market

o South America

§ South America Bone Grafts and Substitutes Market

o Brazil Bone Grafts and Substitutes Market

o Argentina Bone Grafts and Substitutes Market

o Columbia Bone Grafts and Substitutes Market

o South Africa Bone Grafts and Substitutes Market

o Rest of South America Bone Grafts and Substitutes Market

o Middle East and Africa

§ Middle East and Africa Bone Grafts and Substitutes Market

o Saudi Arabia Bone Grafts and Substitutes Market

o UAE Bone Grafts and Substitutes Market

o Egypt Bone Grafts and Substitutes Market

o Nigeria Bone Grafts and Substitutes Market

o South Africa Bone Grafts and Substitutes Market

o Rest of MEA Bone Grafts and Substitutes Market

Table of Contents

1. Introduction

1.1. Report Description

1.2. Research Methodology

1.2.1. Secondary Research

1.2.2. Primary Research

2. Executive Summary

2.1. Key Highlights

3. Market Overview

3.1. Introduction

3.1.1. Market Definition

3.1.2. Market Segmentation

3.2. Market Dynamics

3.2.1. Drivers

3.2.2. Restraints

3.2.3. Opportunities

4. Market Analysis by Regions

4.1. North America (United States, Canada and Mexico)

4.1.1. United States Market States and Outlook (2017-2023)

4.1.2. Canada Market States and Outlook (2017-2023)

4.1.3. Mexico Market States and Outlook (2017-2023)

4.2. Europe (Germany, France, UK, Russia, Italy and Rest of Europe)

4.2.1. Germany Market States and Outlook (2017-2023)

4.2.2. France Market States and Outlook (2017-2023)

4.2.3. UK Market States and Outlook (2017-2023)

4.2.4. Russia Market States and Outlook (2017-2023)

4.2.5. Italy Market States and Outlook (2017-2023)

4.2.6. Rest of Europe Market States and Outlook (2017-2023)

4.3. Asia-Pacific (China, Japan, Korea, India, Southeast Asia and Rest of Asia-Pacific)

4.3.1. China Market States and Outlook (2017-2023)

4.3.2. Japan Market States and Outlook (2017-2023)

4.3.3. Korea Market States and Outlook (2017-2023)

4.3.4. India Market States and Outlook (2017-2023)

4.3.5. Rest of Asia-Pacific Market States and Outlook (2017-2023)

4.4. South America (Brazil, Argentina, Columbia and Rest of South America)

4.4.1. Brazil Market States and Outlook (2017-2023)

4.4.2. Argentina Market States and Outlook (2017-2023)

4.4.3. Columbia Market States and Outlook (2017-2023)

4.4.4. Rest of South America Market States and Outlook (2017-2023)

4.5. Middle East and Africa (Saudi Arabia, UAE, Egypt, Nigeria, South Africa and Rest of MEA)

4.5.1. Saudi Arabia Market States and Outlook (2017-2023)

4.5.2. UAE Market States and Outlook (2017-2023)

4.5.3. Egypt Market States and Outlook (2017-2023)

4.5.4. Nigeria Market States and Outlook (2017-2023)

4.5.5. South Africa Market States and Outlook (2017-2023)

4.5.6. Rest of MEA Market States and Outlook (2017-2023)

5. Bone Grafts and Substitutes Market, By Product

5.1. Introduction

5.2. Global Bone Grafts and Substitutes Revenue and Market Share by Product (2017-2027)

5.2.1. Global Bone Grafts and Substitutes Revenue and Revenue Share by Product (2017-2027)

5.3. Bone Grafts Substitutes

5.3.1. Global Bone Grafts Substitutes Revenue and Growth Rate (2017-2027)

5.4. Cell-based Matrices

5.4.1. Global Cell-based Matrices Revenue and Growth Rate (2017-2027)

5.5. Allografts

5.5.1. Global Allografts Revenue and Growth Rate (2017-2027)

6. Bone Grafts and Substitutes Market, By Application

6.1. Introduction

6.2. Global Bone Grafts and Substitutes Revenue and Market Share by Application (2017-2027)

6.2.1. Global Bone Grafts and Substitutes Revenue and Revenue Share by Application (2017-2027)

6.3. Joint Reconstruction

6.3.1. Global Joint Reconstruction Revenue and Growth Rate (2017-2027)

6.4. Dental Bone Grafting

6.4.1. Global Dental Bone Grafting Revenue and Growth Rate (2017-2027)

6.5. Trauma

6.5.1. Global Trauma Revenue and Growth Rate (2017-2027)

6.6. Craniomaxillofacial

6.6.1. Global Craniomaxillofacial Revenue and Growth Rate (2017-2027)

6.7. Spinal Fusion

6.7.1. Global Spinal Fusion Revenue and Growth Rate (2017-2027)

7. Bone Grafts and Substitutes Market, By Region

7.1. Introduction

7.2. Global Bone Grafts and Substitutes Revenue and Market Share by Regions

7.2.1. Global Bone Grafts and Substitutes Revenue by Regions (2017-2027)

7.3. North America Bone Grafts and Substitutes by Countries

7.3.1. North America Bone Grafts and Substitutes Revenue and Growth Rate (2017-2027)

7.3.2. North America Bone Grafts and Substitutes Revenue by Countries (2017-2027)

7.3.3. North America Bone Grafts and Substitutes Revenue (Million USD) by Countries (2017-2027)

7.3.4. U.S.

7.3.4.1. United States Bone Grafts and Substitutes Revenue (Millions USD) and Growth Rate (2017-2027)

7.3.5. Canada

7.3.5.1. Canada Bone Grafts and Substitutes Revenue (Millions USD) and Growth Rate (2017-2027)

7.3.6. Mexico

7.3.6.1. Mexico Bone Grafts and Substitutes Revenue (Millions USD) and Growth Rate (2017-2027)

7.4. Europe Bone Grafts and Substitutes by Countries

7.4.1. Europe Bone Grafts and Substitutes Revenue and Growth Rate (2017-2027)

7.4.2. Europe Bone Grafts and Substitutes Revenue by Countries (2017-2027)

7.4.3. Europe Bone Grafts and Substitutes Revenue (Million USD) by Countries (2017-2027)

7.4.4. Germany

7.4.4.1. Germany Bone Grafts and Substitutes Revenue (Millions USD) and Growth Rate (2017-2027)

7.4.5. UK

7.4.5.1. UK Bone Grafts and Substitutes Revenue (Millions USD) and Growth Rate (2017-2027)

7.4.6. France

7.4.6.1. France Bone Grafts and Substitutes Revenue (Millions USD) and Growth Rate (2017-2027)

7.4.7. Russia

7.4.7.1. Russia Bone Grafts and Substitutes Revenue (Millions USD) and Growth Rate (2017-2027)

7.4.8. Italy

7.4.8.1. Italy Bone Grafts and Substitutes Revenue (Millions USD) and Growth Rate (2017-2027)

7.4.9. Rest of Europe

7.4.9.1. Rest of Europe Bone Grafts and Substitutes Revenue (Millions USD) and Growth Rate (2017-2027)

7.5. Asia-Pacific

7.5.1. Asia-Pacific Bone Grafts and Substitutes Revenue and Growth Rate (2017-2027)

7.5.2. Asia-Pacific Bone Grafts and Substitutes Revenue by Countries (2017-2027)

7.5.3. Asia-Pacific Bone Grafts and Substitutes Revenue (Million USD) by Countries (2017-2027)

7.5.4. China

7.5.4.1. China Bone Grafts and Substitutes Revenue (Millions USD) and Growth Rate (2017-2027)

7.5.5. Japan

7.5.5.1. Japan Bone Grafts and Substitutes Revenue (Millions USD) and Growth Rate (2017-2027)

7.5.5.2.

7.5.6. Korea

7.5.6.1. Korea Bone Grafts and Substitutes Revenue (Millions USD) and Growth Rate (2017-2027)

7.5.7. India

7.5.7.1. India Bone Grafts and Substitutes Revenue (Millions USD) and Growth Rate (2017-2027)

7.5.8. Southeast Asia

7.5.8.1. Southeast Asia Bone Grafts and Substitutes Revenue (Millions USD) and Growth Rate (2017-2027)

7.5.9. Rest of Asia-Pacific

7.5.9.1. Rest of Asia-Pacific Bone Grafts and Substitutes Revenue (Millions USD) and Growth Rate (2017-2027)

7.6. South America

7.6.1. South America Bone Grafts and Substitutes Revenue and Growth Rate (2017-2027)

7.6.2. South America Bone Grafts and Substitutes Revenue by Countries (2017-2027)

7.6.3. South America Bone Grafts and Substitutes Revenue (Million USD) by Countries (2017-2027)

7.6.4. Brazil

7.6.4.1. Brazil Bone Grafts and Substitutes Revenue (Millions USD) and Growth Rate (2017-2027)

7.6.5. Argentina

7.6.5.1. Argentina Bone Grafts and Substitutes Revenue (Millions USD) and Growth Rate (2017-2027)

7.6.6. Columbia

7.6.6.1. Columbia Bone Grafts and Substitutes Revenue (Millions USD) and Growth Rate (2017-2027)

7.6.7. Rest of South America

7.6.7.1. Rest of South America Bone Grafts and Substitutes Revenue (Millions USD) and Growth Rate (2017-2027)

7.7. Middle East and Africa

7.7.1. Middle East and Africa Bone Grafts and Substitutes Revenue and Growth Rate (2017-2027)

7.7.2. Middle East and Africa Bone Grafts and Substitutes Revenue by Countries (2017-2027)

7.7.3. Middle East and Africa Bone Grafts and Substitutes Revenue (Million USD) by Countries (2017-2027)

7.7.4. Saudi Arabia

7.7.4.1. Saudi Arabia Bone Grafts and Substitutes Revenue (Millions USD) and Growth Rate (2017-2027)

7.7.5. United Arab Emirates

7.7.5.1. United Arab Emirates Bone Grafts and Substitutes Revenue (Millions USD) and Growth Rate (2017-2027)

7.7.6. Egypt

7.7.6.1. Egypt Bone Grafts and Substitutes Revenue (Millions USD) and Growth Rate (2017-2027)

7.7.7. Nigeria

7.7.7.1. Nigeria Bone Grafts and Substitutes Revenue (Millions USD) and Growth Rate (2017-2027)

7.7.8. South Africa

7.7.8.1. South Africa Bone Grafts and Substitutes Revenue (Millions USD) and Growth Rate (2017-2027)

7.7.9. Rest of Middle East and Africa

7.7.9.1. Rest of Middle East and Africa Bone Grafts and Substitutes Revenue (Millions USD) and Growth Rate (2017-2027)

8. Company Profiles

8.1. Arthrex, Inc.

8.1.1. Business Overview

8.1.2. Product Portfolio

8.1.3. Strategic Developments

8.1.4. Revenue and Market Share

8.2. Johnson & Johnson

8.2.1. Business Overview

8.2.2. Product Portfolio

8.2.3. Strategic Developments

8.2.4. Revenue and Market Share

8.3. Baxter International Inc.

8.3.1. Business Overview

8.3.2. Product Portfolio

8.3.3. Strategic Developments

8.3.4. Revenue and Market Share

8.4. Wright Medical Group N.V.

8.4.1. Business Overview

8.4.2. Product Portfolio

8.4.3. Strategic Developments

8.4.4. Revenue and Market Share

8.5. Xtant Medical Holdings, Inc.

8.5.1. Business Overview

8.5.2. Product Portfolio

8.5.3. Strategic Developments

8.5.4. Revenue and Market Share

8.6. Zimmer Biomet Holdings, Inc.

8.6.1. Business Overview

8.6.2. Product Portfolio

8.6.3. Strategic Developments

8.6.4. Revenue and Market Share

8.7. Medtronic Plc.

8.7.1. Business Overview

8.7.2. Product Portfolio

8.7.3. Strategic Developments

8.7.4. Revenue and Market Share

8.8. Stryker Corporation

8.8.1. Business Overview

8.8.2. Product Portfolio

8.8.3. Strategic Developments

8.8.4. Revenue and Market Share

8.9. Musculoskeletal Transplant Foundation

8.9.1. Business Overview

8.9.2. Product Portfolio

8.9.3. Strategic Developments

8.9.4. Revenue and Market Share

8.10. Integra Lifesciences Holdings Corporation

8.10.1. Business Overview

8.10.2. Product Portfolio

8.10.3. Strategic Developments

8.10.4. Revenue and Market Share

9. Global Bone Grafts and Substitutes Market Competition, by Manufacturer

9.1. Global Bone Grafts and Substitutes Revenue and Market Share by Manufacturer (2017-2017)

9.2. Global Bone Grafts and Substitutes Price by Region (2017-2017)

9.3. Top 5 Bone Grafts and Substitutes Manufacturer Market Share

9.4. Market Competition Trend

10. Bone Grafts and Substitutes Market Forecast (2027-2023)

10.1. Global Bone Grafts and Substitutes Revenue (Millions USD) and Growth Rate (2027-2023)

10.2. Bone Grafts and Substitutes Market Forecast by Regions (2027-2023)

10.2.1. North America Bone Grafts and Substitutes Market Forecast (2027-2023)

10.2.1.1. United States Bone Grafts and Substitutes Market Forecast (2027-2023)

10.2.1.2. Canada Bone Grafts and Substitutes Market Forecast (2027-2023)

10.2.1.3. Mexico Bone Grafts and Substitutes Market Forecast (2027-2023)

10.2.2. Europe Bone Grafts and Substitutes Market Forecast (2027-2023)

10.2.2.1. Germany Bone Grafts and Substitutes Market Forecast (2027-2023)

10.2.2.2. United Kingdom Bone Grafts and Substitutes Market Forecast (2027-2023)

10.2.2.3. France Bone Grafts and Substitutes Market Forecast (2027-2023)

10.2.2.4. Russia Bone Grafts and Substitutes Market Forecast (2027-2023)

10.2.2.5. Italy Bone Grafts and Substitutes Market Forecast (2027-2023)

10.2.2.6. Rest of the Europe Bone Grafts and Substitutes Market Forecast (2027-2023)

10.2.3. Asia-Pacific Bone Grafts and Substitutes Market Forecast (2027-2023)

10.2.3.1. China Bone Grafts and Substitutes Market Forecast (2027-2023)

10.2.3.2. Japan Bone Grafts and Substitutes Market Forecast (2027-2023)

10.2.3.3. Korea Bone Grafts and Substitutes Market Forecast (2027-2023)

10.2.3.4. India Bone Grafts and Substitutes Market Forecast (2027-2023)

10.2.3.5. Southeast Asia Bone Grafts and Substitutes Market Forecast (2027-2023)

10.2.3.6. Rest of Asia-Pacific Bone Grafts and Substitutes Market Forecast (2027-2023)

10.2.4. South America Bone Grafts and Substitutes Market Forecast (2027-2023)

10.2.4.1. Brazil Bone Grafts and Substitutes Market Forecast (2027-2023)

10.2.4.2. Argentina Bone Grafts and Substitutes Market Forecast (2027-2023)

10.2.4.3. Columbia Bone Grafts and Substitutes Market Forecast (2027-2023)

10.2.4.4. Rest of South America Bone Grafts and Substitutes Market Forecast (2027-2023)

10.2.5. Middle East and Africa Bone Grafts and Substitutes Market Forecast (2027-2023)

10.2.5.1. Saudi Arabia Bone Grafts and Substitutes Market Forecast (2027-2023)

10.2.5.2. UAE Bone Grafts and Substitutes Market Forecast (2027-2023)

10.2.5.3. Egypt Bone Grafts and Substitutes Market Forecast (2027-2023)

10.2.5.4. Nigeria Bone Grafts and Substitutes Market Forecast (2027-2023)

10.2.5.5. South Africa Bone Grafts and Substitutes Market Forecast (2027-2023)

10.2.5.6. Rest of MEA Bone Grafts and Substitutes Market Forecast (2027-2023)

10.3. Bone Grafts and Substitutes Market Forecast by Product (2027-2023)

10.3.1. Global Bone Grafts and Substitutes Revenue Forecast by Product (2027-2023)

10.3.2. Global Bone Grafts and Substitutes Revenue Market Share Forecast by Product (2027-2023)

10.4. Bone Grafts and Substitutes Market Forecast by Application (2027-2023)

10.4.1. Global Bone Grafts and Substitutes Revenue Forecast by Application (2027-2023)

10.4.2. Global Bone Grafts and Substitutes Revenue Market Share Forecast by Application (2027-2023)

List of Tables

*You can glance through the list of Tables and Figures when you view the sample copy of Bone Grafts and Substitutes Market.

Research Methodology

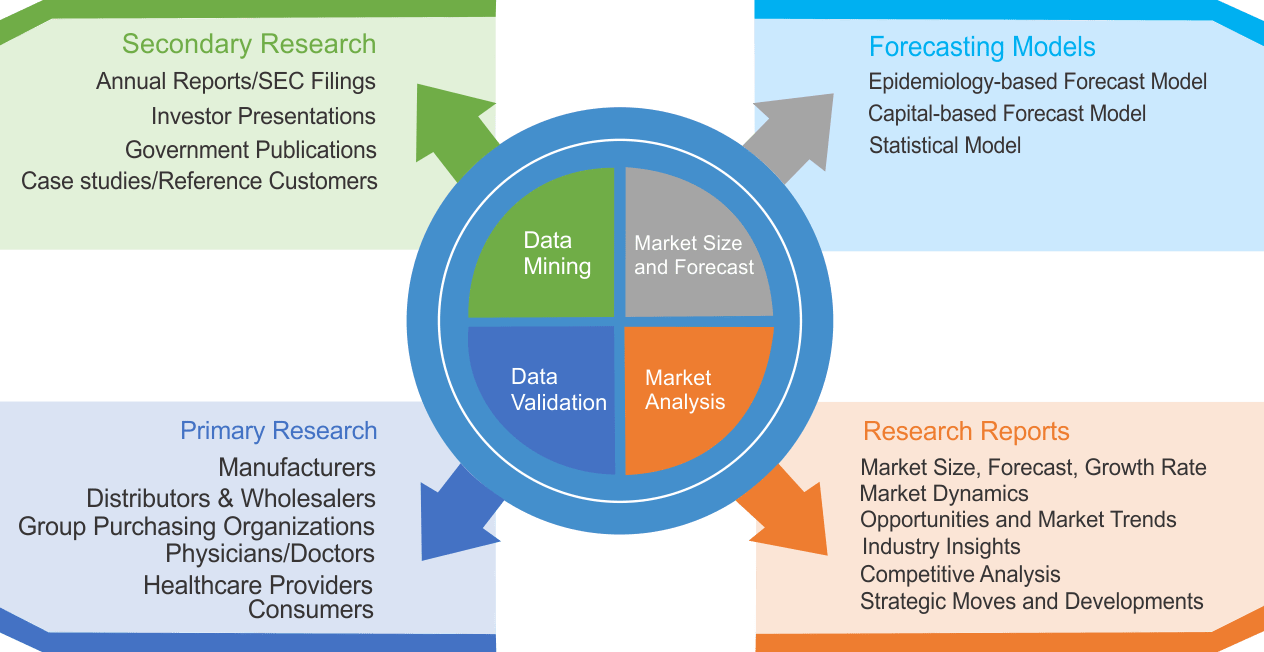

We use both primary as well as secondary research for our market surveys, estimates and for developing forecast. Our research process commence by analyzing the problem which enable us to design the scope for our research study. Our research process is uniquely designed with enough flexibility to adjust according to changing nature of products and markets, while retaining core element to ensure reliability and accuracy in research findings. We understand both macro and micro-economic factors to evaluate and forecast different market segments.

Data Mining

Data is extensively collected through various secondary sources such as annual reports, investor presentations, SEC filings, and other corporate publications. We also refer trade magazines, technical journals, paid databases such as Factiva and Bloomberg, industry trade journals, scientific journals, and social media data to understand market dynamics and industry trends. Further, we also conduct primary research to understand market drivers, restraints, opportunities, challenges, and competitive scenario to build our analysis.

Data Collection Matrix

|

Data Collection Matrix |

Supply Side |

Demand Side |

|

Primary Data Sources |

|

|

|

Secondary Data Sources |

|

|

Market Modeling and Forecasting

We use epidemiology and capital equipment-based models to forecast market size of different segments at country and regional level.

- Epidemiology-based Forecasting Model: This method uses epidemiology data gathered through various publications and from physicians to estimate population of patients, flow of treatment of individual disease and therapies. The data collected through this method includes statics on incidence of disease, population suffering from disease, and treatment population. This method is used to understand:

- Number of patients for particular device or medical procedure and

- Repeated use of particular device depending on health and condition of patient

- Capital-based Forecasting Model: This method of forecasting is based on number of replacements, installed-based and new sales of capital equipment used in various healthcare and diagnostic centers. These three parameters are calculated and forecast is developed. Installation base is calculated as average number of units per facility; while sales for particular year is calculated from number of new and replace units. Secondary data is collected through various supply chain intermediaries and opinion leaders to arrive at installation and sales rate. These techniques help our analysts in validating market and developed market estimates and forecast.

We do forecast on basis of several parameters such as market drivers, market opportunities, industry trends government regulations, raw materials supply and trade dynamics to ensure relevance of forecast with market scenario. With increasing need to granulized information, we used bottom-up methodology for forecasting where we evaluate each regional segment differently and combined all forecast to develop final market forecast.

Data Validation

We believe primary research is a very important tool in analyzing and forecasting different markets. In order to make sure accuracy of our findings, our team conducts primary interviews at every stage of research to gain deep insights into current business environment and future trends and key developments in market. This includes use of various methods such as telephonic interviews, focus groups, face to face interviews and questionnaires to validate our research from all aspects. We validate our data through primary research from key industry leaders such as CEO, product managers, marketing managers, suppliers, distributors, and consumers are frequently interviewed. These interviews provide valuable insights which help us to have better market understanding besides validating our estimates and forecast.

Data Triangulation

Industry Analysis

|

Qualitative Data |

Quantitative Data (2017-2025) |

|

|